ESG incidents and value destruction: insights from the Sustainalytics incidents integration study

February 22, 2018

New analysis from Sustainalytics indicates that incidents and, in particular, high- and severe-impact incidents, are associated with important share price effects. The authors of this report outline some of the findings.

Corporate activities that generate undesirable social or environmental effects are a valuable source of information for investors. Environmental, social and governance (ESG) incidents can reflect gaps in a company’s management systems, vulnerabilities in corporate strategy and lapses in policy development, all of which are highly relevant to company analysis and evaluation. If policies and programmes are the talk of corporate ESG management, then incidents are the walk.

Incidents can also have direct financial effects. Many well-known examples of shareholder value destruction over the last few years, including product safety concerns at Samsung, the Dakota Access Pipeline controversy and the Volkswagen emissions scandal, were all “incidents” in Sustainalytics’ terminology.

Focusing on the essential trends

In our recently published study, Understanding ESG incidents: key lessons for investors, we analyse 29,000 incidents that took place in 176 countries from 2014-2016. We identify the essential incident trends, including those related to company size, industry classifications and geographical considerations.

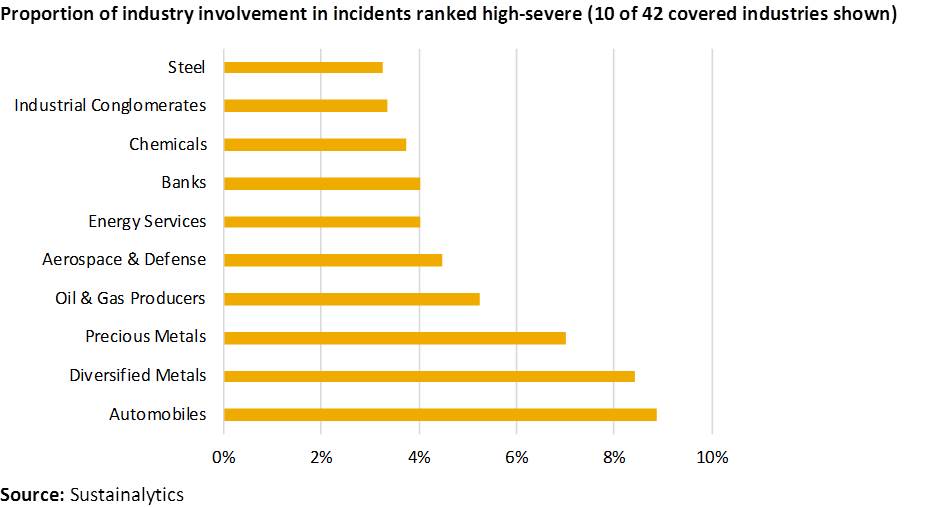

One of the key industry trends we observe is that automobile companies comprise the most incident-prone industry in our coverage universe. During our study period, 52% of all covered auto firms were involved in incidents. What’s more, 9% of these companies were involved in incidents ranked high-severe, making the automobiles industry more exposed to high-impact incidents than any other industry (see figure below). The 2015 Volkswagen emissions scandal is just one example of a high-impact incident linked to this industry.

The financial materiality of incidents

Determining the financial impact of incidents is an obviously complex exercise. The simplified approach that we developed for this study does not purport to be entirely conclusive or establish a causal relationship between incidents and financial performance. However, our findings provide a compelling foundation for deeper research.

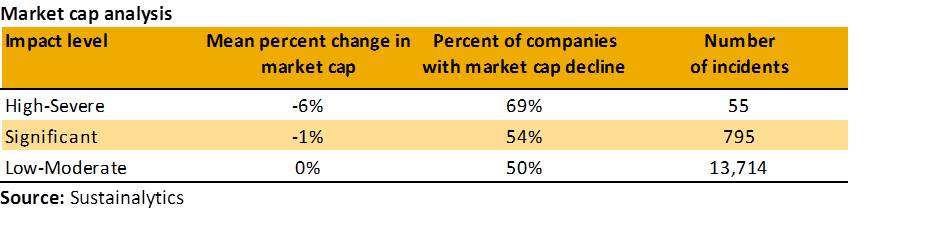

Our methodology involves studying more than 14,000 initial incidents drawn from the larger dataset and comparing the market cap value of companies five days before and five days after an incident. The results are presented in the table below.

Our analysis indicates that incidents and, in particular, high- and severe-impact incidents, are associated with important share price effects. Over two-thirds (69%) of companies that experienced a high-severe incident also experienced a market cap decline during the ten-day incident window, with an average decline of 6%.

Applying the findings and maximizing engagement impact

The relatively high exposure of the automobiles industry to incidents, especially those ranked high-severe, raises the question of how investors can mitigate their exposure to the industry. We present several examples of how to integrate our findings in the report, including industry tilts, blending incident data with beta analysis, portfolio construction and engagement processes. Each of these applications exemplifies some of the unique benefits of integrating ESG incidents data into the investment decision-making process.

During the webinar series for this study, several audience participants expressed an interest in our idea of developing an “incident-driven engagement” process. This is the idea is that investors can incorporate incident analysis in their issue selection process. As shown in the table below, there appears to be a disconnect between the most common ESG engagement issues and the top incident-driven candidates.

Granted, engagement issues tend to be much broader and, in many cases, more systemically important than a single incident category. Nevertheless, using a simple ranking system that recognizes incident frequency and impact, investors could potentially maximize the real-world impact of their engagement efforts by expanding their conversations with management to include incidents.

Further research on the horizon

We will continue to analyze the growing Sustainalytics incident universe, monitor the market and experiment with other applications of the findings. Since we found that high-impact incidents are associated with especially pronounced market effects, we plan to explore new ways of integrating this finding into the investment process.

For example, the list of top incident-engagement processes noted in the table above are driven by a combination incident frequency and impact considerations, while our portfolio analysis was driven primarily by the frequency of companies’ ESG incidents. In the next iteration of our portfolio analysis, we may apply additional factors to the selection process, including the impact level of each company’s ESG incidents, which may help investors identify the best incident performers with an emphasis on excluding firms associated with particularly high impact incidents.

Doug Morrow, Martin Vezér, Andrei Apostol and Kasey Vosburg are the authors of Sustainalytics’ recent thematic report, Understanding ESG incidents: key lessons for investors.

COMMENTS